When Americans move to the UK and sort out their IRS filing, they often forget a second layer entirely: US state tax. Some states keep treating you as a taxpayer long after you have left the country — and unlike federal tax, there is no US/UK treaty and no Foreign Tax Credit to soften a state bill. A handful of aggressive 'sticky states' are the worst offenders. Here is which states still claim you, how the rules work, and how to cut ties cleanly before — or after — you move. We will cover why state tax sits outside the treaty, the five states that fight hardest to keep you, how domicile differs from residency, the steps that draw a clean line under your state residency, and the common mistakes that quietly keep an old state on your back for years.

Why state tax is a separate problem

US tax has two layers: federal (the IRS) and state. The reliefs that protect Americans abroad from double taxation — the Foreign Earned Income Exclusion, the Foreign Tax Credit, and the US/UK tax treaty — are all federal. States are not party to the treaty and mostly do not give credit for foreign tax. So a state can still consider you a resident and tax your worldwide income even when the IRS, thanks to the treaty, collects nothing.

This catches people out because they reasonably assume that leaving the country ends all their US obligations. For federal purposes it does not (citizenship-based taxation), and for some states it does not either — for a different reason: domicile.

Domicile vs residency: the key distinction

Most sticky-state problems come down to domicile. Your domicile is your true, fixed, permanent home — the place you intend to return to, even if you are living elsewhere for now. You can be physically resident in the UK while a US state still treats you as domiciled there, and therefore still taxable.

States look at a bundle of factors to decide whether you have genuinely given up your domicile: where you keep a home, your driver's licence, voter registration, vehicle registration, bank and brokerage accounts, professional licences, where your family is, and where you say you intend to return. New York in particular distinguishes residency from domicile and can tax you on the strength of domicile alone, even with minimal time in the state.

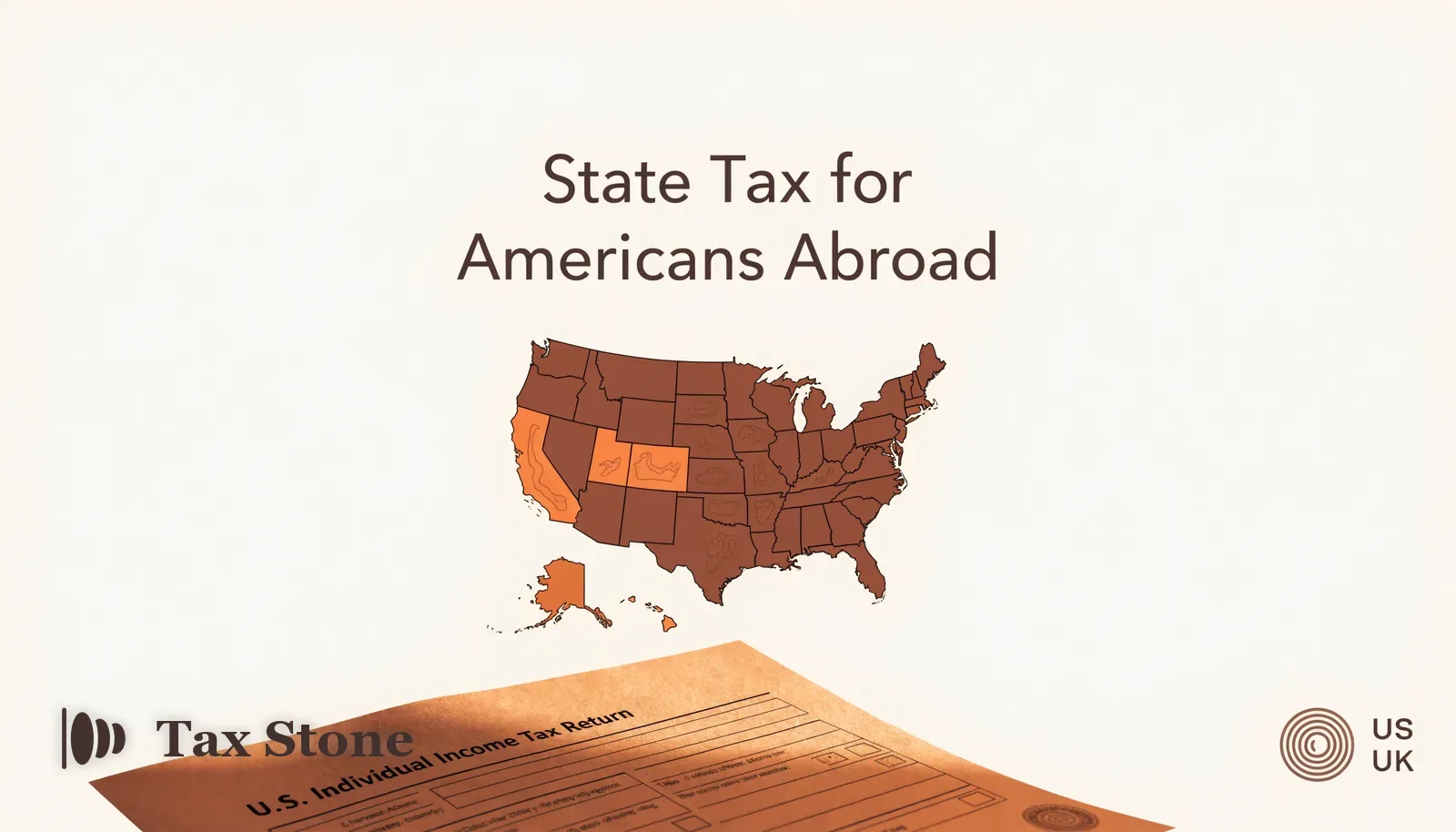

The 'sticky states' to watch

Five states are notorious for making it hard to shake off tax residency once you move abroad. If you last lived in one of these, assume you have a state question to resolve:

- California — aggressive on continued residency and domicile; keeps taxing former residents who retain ties.

- New York — taxes on domicile, distinguishing it from physical residency; very sticky.

- Virginia — difficult to break residency; looks closely at intent and ties.

- South Carolina — also treats domicile tenaciously.

- New Mexico — another state that holds on to former residents.

How states determine whether you must file

Broadly, a state can tax you if you are still domiciled there, if you meet a statutory residency test (often based on days present and maintaining an abode), or if you have state-sourced income. Even after you have genuinely left, state-sourced income — such as rent from a property you still own in the state, or income from a business based there — can keep you on the hook for a state return on that income, regardless of where you live.

The practical upshot: your state obligation depends on your specific facts and your last state of residence. Two Americans in London, one from Texas and one from California, can have completely different state positions.

States with no income tax

On the bright side, several US states have no state income tax at all, including Florida, Texas, Washington, Nevada, Tennessee, Wyoming, South Dakota and Alaska. If your last state of residence was one of these, you generally have no state filing obligation when you move abroad. This is also why some Americans planning a long move abroad deliberately establish residency in a no-tax state before they leave — though doing so has to be genuine, not a paper exercise. A word of caution even here: a couple of these states still tax certain investment income or have historically done so, and moving your stated residency without genuinely relocating your life can be challenged, so the 'no-tax state' route works best when it reflects a real change rather than a mailbox.

How to cut state ties cleanly

If you are leaving a sticky state, the goal is to demonstrate a clear, genuine change of domicile to the UK. The more of these you do, the stronger your position:

- Sell or rent out your home in the state (and clearly establish your UK home as primary).

- Surrender or change your state driver's licence; register to drive in the UK.

- Cancel state voter registration.

- Move bank and brokerage accounts away from the state where practical, and update your address.

- Cancel state-based memberships, and keep evidence of your UK ties (lease, council tax, employment).

- File a final part-year resident state return for the year you leave, showing the departure date.

No treaty, no Foreign Tax Credit — so it can really cost

It bears repeating because it surprises people: the US/UK treaty does not bind US states, and most states do not give a credit for UK tax. So if California still considers you resident, it can tax your UK salary with no offset for the UK tax you have already paid — genuine double taxation that the federal system would have prevented. That is why resolving a sticky-state position is often more financially urgent than the federal return, which the Foreign Tax Credit usually reduces to zero.

What to do before you move (or now, if you've already left)

The cleanest time to deal with state tax is before you leave: establish the change of domicile, file your final part-year return, and cut ties deliberately. If you have already moved and never addressed it, it is worth checking whether your old state still considers you a resident — and, if so, correcting your position before the bills and interest mount up. A US tax specialist in the UK can review your last state of residence and tell you whether you still have an obligation.

A tale of two expats: California vs Texas

The difference the right state makes is stark. Picture two Americans who move to London in the same month on identical UK salaries. The first last lived in Texas, which has no state income tax; she has no state filing obligation at all, and her US compliance is purely federal. The second last lived in California and kept a condo, a California driver's licence and a California brokerage account; California may well still treat him as a resident, taxing his UK salary with no credit for the UK tax he has already paid.

Same job, same city, same income — but one has a clean federal-only position and the other faces real, unrelieved double taxation until he resolves his California residency. That is the practical power of domicile, and why your last US state matters as much as your visa or your salary.

Filing a final part-year state return

A key step in cleanly ending a state obligation is filing a final part-year resident return for the year you leave. This return reports your income up to your departure date and signals to the state that you have moved and ceased residency. Skipping it can leave the state assuming you are still a full-year resident, which is exactly how lingering liabilities and notices arise. Filing it properly — with a clear departure date and consistent supporting facts (UK lease, employment, the ties you cut) — draws a line under your residency and is far easier than arguing the point years later.

Common state-tax mistakes Americans abroad make

Most state-tax problems are avoidable and come from a handful of recurring errors. Knowing them in advance is half the battle:

- Assuming the federal reliefs cover state tax — they do not; the FEIE, Foreign Tax Credit and treaty are all federal.

- Keeping a sticky-state driver's licence, voter registration or address 'for convenience' — each is evidence of continued domicile.

- Never filing a final part-year return, so the state assumes you are still a full-year resident.

- Forgetting about state-sourced income — rent from a property or income from a business in the state can keep you filing there even after a clean move.

- Believing that paying UK tax automatically settles any US state bill — most states give no credit for foreign tax.

The bottom line

Federal compliance is only half the US picture. Before you assume your only American filing is the IRS, identify your last state of residence, check whether it is a sticky state, and make sure you have genuinely broken domicile. For most people from no-tax states there is nothing to do; for those from California, New York, Virginia, South Carolina or New Mexico, a little planning can save years of unnecessary — and unrelieved — state tax. If you are unsure where you stand, our broader guide to how US tax returns work for Americans in the UK puts the state question in context.